What Is a Central Bank Digital Currency (CBDC)?

Imagine a world where the cash in your pocket no longer exists in physical form but as a secure, digital currency that you can access anytime, anywhere, with just a smartphone or computer. This future is closer than you might think, as Central Bank Digital Currencies (CBDCs) are gaining momentum around the globe. As of now, over 130 countries—representing more than 95% of the global GDP—are exploring or piloting CBDCs, signaling a revolutionary shift in the way we think about money. But what exactly are CBDCs, and how will they change our financial systems, daily transactions, and even the role of traditional banks?

This article explores what CBDCs are, how they work, the potential benefits they offer, the challenges they pose, and how they are shaping the future of money.

What Is Fiat Money and Why Is It Important for CBDCs?

To fully understand CBDCs, it’s important to first grasp the concept of fiat money. Fiat money refers to a currency that has no intrinsic value but is deemed valuable because a government declares it to be legal tender. Unlike commodities like gold or silver, which have inherent value, fiat money gets its worth from the stability and authority of the government behind it. The U.S. dollar, the euro, and the British pound are all examples of fiat money, and they are universally accepted as a means of payment.

CBDCs are digital versions of this same fiat money, but with a crucial difference: while physical cash is becoming less popular, digital currencies are taking over as the preferred mode of payment. Central banks are exploring CBDCs to create digital currencies that will continue to carry the same legal weight as paper money but in a more modern, efficient format. CBDCs aim to offer the same level of trust, stability, and security that fiat currencies have, while providing the convenience of a digital, faster, and more secure payment system.

What Is a Central Bank Digital Currency (CBDC)?

A Central Bank Digital Currency, or CBDC, is a digital form of a nation's official currency issued and regulated by the central bank. Unlike cryptocurrencies such as Bitcoin, which operate independently on decentralized networks using blockchain technolog, CBDCs are centralized and are fully backed by the authority and trust of the central bank. This makes them legal tender, meaning they must be accepted for payment for all debts and financial obligations within a country.

CBDCs are designed to work within the existing financial system, and their primary purpose is to make digital payments safer, faster, and more efficient. While physical cash remains essential in many parts of the world, digital payments are growing at an exponential rate. In fact, global mobile payments are projected to surpass $26.53 trillion by 2032. As cash usage declines, the need for a reliable and secure digital currency backed by the government has become more pressing. CBDCs are the answer to this growing demand for digital currency solutions.

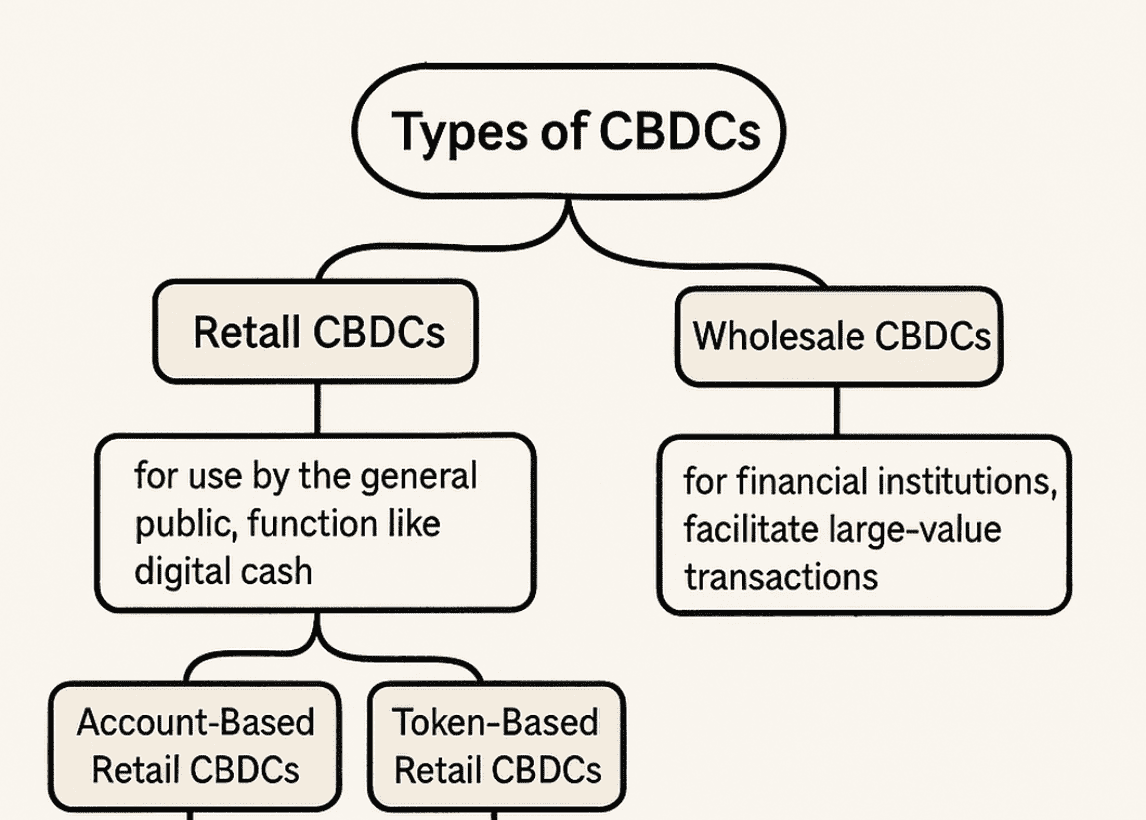

Types of CBDCs

There are two main types of CBDCs: retail CBDCs and wholesale CBDCs. Both types aim to modernize payment systems, but they serve different purposes and target different users.

Retail CBDCs

Retail CBDCs are digital currencies designed for use by the general public, including consumers and businesses. These digital currencies function like cash but in digital form. They are intended to be used for everyday transactions, such as paying for goods and services, transferring money between individuals, or making online purchases. Retail CBDCs can be accessed through digital wallets or mobile apps linked to an individual’s bank account.

Retail CBDCs can be further divided into two types:

-

Account-Based Retail CBDCs: In this system, users hold accounts directly with the central bank or through authorized intermediaries, such as commercial banks. Transactions are recorded in centralized databases, and access to the currency is secured by personal identification methods. This model allows central banks to monitor transactions more closely and ensure compliance with regulatory standards, but it may raise concerns about privacy and data security.

-

Token-Based Retail CBDCs: In this model, users hold digital tokens that represent units of the currency. These tokens can be transferred peer-to-peer, much like physical cash, and transactions are designed to be anonymous and decentralized. Token-based CBDCs aim to offer the privacy of cash transactions while retaining the security of digital payments.

Wholesale CBDCs

Wholesale CBDCs are digital currencies designed primarily for financial institutions, such as commercial banks and payment processors. These currencies facilitate large-value transactions and improve the efficiency of interbank payments and settlements. Wholesale CBDCs are primarily used by financial entities to conduct large-scale transactions more securely, reducing settlement times and lowering transaction costs, especially for cross-border payments.

While wholesale CBDCs won’t be used by the general public, they are critical in improving the overall efficiency of the financial system. They help streamline processes and enable faster and more secure transactions between financial institutions.

How CBDCs Work

CBDCs are not simply digital versions of cash; they are designed to offer a range of benefits and features that set them apart from traditional currencies.

Centralized Control

The most defining feature of a CBDC is that it is centralized. This means that the central bank or government has complete control over the issuance, distribution, and regulation of the currency. In contrast, cryptocurrencies like Bitcoin are decentralized, meaning they are not controlled by any central authority. Centralized control ensures that CBDCs can be integrated into existing monetary systems and allow for the implementation of monetary policies.

Digital Nature

CBDCs exist only in digital form, meaning they do not have a physical counterpart like banknotes or coins. This makes them easier to use and transfer, particularly in a world that is increasingly reliant on digital payments. As digital assets, CBDCs can be easily stored in digital wallets and transferred electronically between individuals, businesses, and institutions. The digital nature of CBDCs also allows for faster and more efficient transactions, which is particularly important in the context of an increasingly globalized and interconnected economy.

Legal Tender Status

CBDCs are considered legal tender, which means they are recognized by law as an official form of payment. This gives them the same status as physical currency, meaning they can be used to settle debts and financial obligations within a country. While cryptocurrencies are not recognized as legal tender in most countries, CBDCs would have the force of law behind them, making them universally accepted within the national economy.

Security and Privacy

Security is a key feature of CBDCs. Central banks and governments are keen to ensure that CBDCs are secure from fraud, hacking, and other cyber threats. Advanced cryptographic techniques are used to protect CBDC transactions, ensuring that they are tamper-proof and traceable. However, privacy is a key consideration as well. While CBDCs offer greater security than physical currency, the degree of privacy they afford users may vary depending on the type of CBDC and the regulatory framework governing it.

The Benefits of CBDCs

Improved Payment Efficiency

CBDCs could make payment systems more efficient by reducing transaction costs and settlement times. Unlike traditional payment methods, which require intermediaries such as banks or payment processors, CBDCs would allow for direct transactions between users and central banks, eliminating these intermediaries and speeding up the payment process.

Financial Inclusion

CBDCs have the potential to improve financial inclusion by providing digital access to money for people who are unbanked or underbanked. According to the World Bank, approximately 1.4 billion adults globally do not have access to a bank account. By offering a digital alternative to cash, CBDCs can provide people with a safe, secure, and easily accessible means of participating in the financial system.

Enhanced Monetary Policy

CBDCs provide central banks with new tools for implementing monetary policy. By having a digital currency that can be directly monitored and regulated, central banks can more easily control the money supply, manage inflation, and implement measures such as negative interest rates or direct stimulus payments.

Reduced Risk of Financial Crimes

Since CBDC transactions are traceable and recorded on secure digital ledgers, they could help reduce the risk of money laundering, tax evasion, and other financial crimes. Governments could more easily track and monitor transactions, making it harder for criminals to use the financial system for illicit activities.

The Challenges of CBDCs

Despite their potential benefits, CBDCs also come with several challenges and risks that must be addressed:

Privacy Concerns

One of the primary concerns surrounding CBDCs is the potential loss of privacy. Unlike cash, which is anonymous, CBDC transactions could be monitored by governments and central banks. This raises concerns about surveillance and the potential for misuse of personal financial data.

Cybersecurity Risks

As digital assets, CBDCs are susceptible to cyberattacks and fraud. Ensuring the security of CBDC systems will be critical to their success. Any breach or hack could undermine public trust in the system and potentially lead to financial instability.

Impact on Traditional Banks

The introduction of CBDCs could disrupt the traditional banking system. If consumers and businesses shift their deposits from commercial banks to digital wallets, it could affect the ability of banks to lend and create credit, potentially leading to liquidity issues.

Implementation Costs

Developing and implementing CBDCs involves significant costs, including investments in technology, infrastructure, and regulatory frameworks. Governments and central banks will need to ensure that the benefits outweigh the costs and that the system is accessible and user-friendly for everyone.

The Global Race to Launch CBDCs

If you wonder, has any country launched a CBDC yet? The answer is yes—several countries have already introduced Central Bank Digital Currencies (CBDCs). As of early 2025, the following nations have rolled out their own digital currencies:

-

The Bahamas: Launched the "Sand Dollar" in October 2020, becoming the first country to issue a CBDC.

-

Jamaica: Introduced the "Jam-Dex" in July 2022, recognizing it as legal tender.

-

Nigeria: Launched the "e-Naira" in October 2021, aiming to enhance financial inclusion and payment efficiency.

-

China: Developed the digital yuan, also known as the digital renminbi (e-CNY), with extensive pilot programs and trials across various cities.

India: Initiated the "Digital Rupee" pilot project in November 2022, with plans for broader implementation. -

Russia: Launched the "Digital Ruble" pilot program, aiming to modernize the payment system.

-

Brazil: Developed the "Drex," with testing phases initiated in March 2023.

-

Eastern Caribbean Currency Union (ECCU): Introduced "DCash" in March 2021, serving multiple island nations.

-

Sweden: Launched the "e-krona" pilot project to explore digital currency options.

-

South Korea: Initiated the "Digital Won" pilot program to assess the feasibility of a digital currency.

-

United Arab Emirates: Developed the "Digital Dirham" as part of a broader CBDC strategy.

CBDCs vs. Cryptocurrencies

Central Bank Digital Currencies (CBDCs) and cryptocurrencies are both exciting developments in the world of digital money, but they each come with their own unique flavor. CBDCs are like a digital version of the cash you already know and use, but with a twist—these are issued and controlled by a country's central bank. This means they’re officially recognized as legal tender and are backed by the government, making them stable and secure. Countries like China and the Bahamas have already launched their own CBDCs, with more countries jumping on board, eager to modernize their financial systems and make payments faster and more inclusive.

Cryptocurrencies, on the other hand, are the rebels of the digital currency world. With names like Bitcoin and Ethereum, they run on decentralized networks, meaning there’s no government or central bank in charge. Instead, transactions are validated by a global network of computers using blockchain technology. While this gives cryptocurrencies a lot of freedom and privacy, it also comes with some wild price swings. One minute, the value could skyrocket, and the next, it could plummet. For some, the risk is worth the reward, but for others, it’s a bit too unpredictable. So, while CBDCs offer stability and government backing, cryptocurrencies offer freedom and the potential for big gains—or losses.

Conclusion

Central Bank Digital Currencies represent a significant evolution in the digitalization of money, offering potential benefits such as improved payment efficiency, financial inclusion, and enhanced monetary policy tools. However, they also present challenges related to privacy, cybersecurity, and financial stability. As countries continue to explore and develop CBDCs, careful consideration of these factors will be essential to ensure that the advantages are realized while mitigating potential risks. The future of money is digital, and CBDCs could play a central role in shaping that future.

Disclaimer: The opinions expressed in this article are for informational purposes only. This article does not constitute an endorsement of any of the products and services discussed or investment, financial, or trading advice. Qualified professionals should be consulted prior to making financial decisions.